Building a Stock Market Agent

I wanted to see if I could build a stock market agent leveraging

open source models, ollama, Python, and real stock market data.

The agent should accept a persona in plain-text which describes

it trading strategy. The agent will begin with a fixed amount of

cash which it can use to buy and sell three different stocks:

| Risk Level | Stock Ticker | Rationale |

| Low Risk | VOO |

A broad market indicator considered safe |

| Medium Risk | NVDA |

A high performance, but somewhat risky tech stock |

| High Risk | SMCI |

An extremely volatile tech stock |

At each turn (representing one week of trading) I take the closing price of each of these stocks and allow the agent to buy, sell, or hold its position based on new market data. It also has history of recent trades and current market prices.

This leverages pydantic and structured output to validate the

JSON output. It ensures the LLM responds using only a valid set

of possible responses using the BaseModel.

import tqdm

import ollama

import yfinance

import polars as pl

import plotnine as p9

from typing import Literal

from pydantic import BaseModel, Field

MODEL = "llama3.2"

MIN_DATE = "2025-01-01"

MAX_DATE = "2026-03-31"

#### Prepare Stock Data ####

market_data = (

yfinance.download(

tickers=["VOO", "NVDA", "SMCI"],

start=MIN_DATE,

end=MAX_DATE,

progress=False,

interval="1wk"

)

.get("Close")

.reset_index()

.pipe(pl.DataFrame)

.sort("Date")

.select(

pl.col("Date").dt.to_string("%Y-%m-%d").alias("date"),

pl.col("VOO").round(2).alias("LOW_RISK"),

pl.col("NVDA").round(2).alias("MED_RISK"),

pl.col("SMCI").round(2).alias("HIGH_RISK"),

)

.iter_rows(

named=True

)

)

#### Define Agent Behavior ####

class Decision(BaseModel):

ticker: Literal["LOW_RISK", "MED_RISK", "HIGH_RISK"]

action: Literal["BUY", "SELL", "HOLD"]

quantity: int = Field(description="Must be 0 if holding.")

class Agent:

def __init__(self, persona: str):

self.persona = persona

self.cash = 10000.0

self.shares = {"LOW_RISK": 0, "MED_RISK": 0, "HIGH_RISK": 0}

self.history = []

self.portfolio_value = []

def advance(self, stock_prices: dict):

# We only feed the last 3 logs to keep context window overhead minimal

prompt = f"""

Output your next trading decision. Maximize

the value of your portfolio.

Strategy: {self.persona}

Balances: Cash ${self.cash:.2f} | Shares {self.shares}

Market Prices: { {k: v for k, v in stock_prices.items() if k != 'date'} }

Recent Actions: {self.history[-3:]}

"""

response = ollama.chat(

model=MODEL,

messages=[{"role": "user", "content": prompt}],

format=Decision.model_json_schema()

)

order = Decision.model_validate_json(response.message.content)

price = stock_prices[order.ticker]

if order.action == "BUY" and self.cash >= order.quantity * price:

self.cash -= order.quantity * price

self.shares[order.ticker] += order.quantity

self.history.append(f"{stock_prices}: Bought {order.quantity} {order.ticker}")

elif order.action == "SELL" and self.shares[order.ticker] >= order.quantity:

self.shares[order.ticker] -= order.quantity

self.cash += order.quantity * price

self.history.append(f"{stock_prices}: Sold {order.quantity} {order.ticker}")

else:

self.history.append(f"{stock_prices}: Held positions")

# Portfolio total value calculation (Cash + Asset Value)

asset_value = sum(self.shares[i] * stock_prices[i] for i in self.shares)

self.portfolio_value.append(round(self.cash + asset_value, 2))

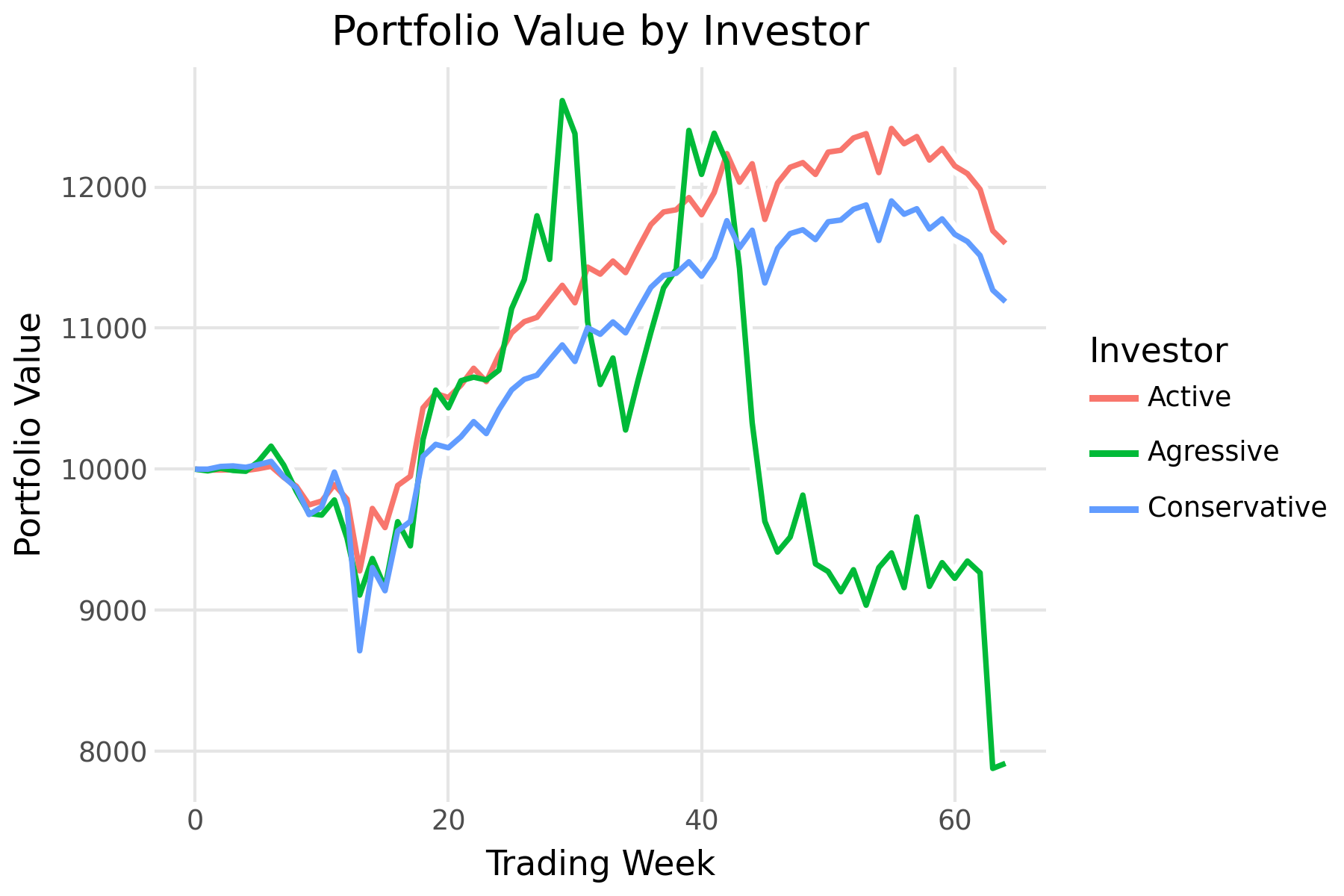

Next we run the simulation! I ran this over a 1.25 year period starting in 2025 Q1 and ending in 2026 Q1. You can see the three personas defined here:

agents = {

"Conservative": Agent("Holds low risk stocks over long periods and does not trade often"),

"Active": Agent("A modest investor who occasionally trades"),

"Aggressive": Agent("A high risk investor who makes frequent trades")

}

for stock_prices in tqdm.tqdm(market_data):

for label, agent in agents.items():

agent.advance(stock_prices)

Finally, we visualize the results. We can see that the conservative agent made few trades generally holding VOO throughout the simulation. The medium-risk agent made a few more trades and the high-risk agent traded often!

The conservative agent performed only slightly worse than the moderate agent. Meanwhile, the aggressive agent made significant gains before losing their portfolio during market volatility.

results = (

pl.DataFrame({

k: v.portfolio_value

for k, v in agents.items()

})

.with_row_index("day")

.unpivot(

index="day"

)

)

plot = (

p9.ggplot(

data=results,

mapping=p9.aes(

x="day",

y="value",

color="variable",

group="variable"

)

) +

p9.geom_line(

size=3,

color="white"

) +

p9.geom_line(

size=1

) +

p9.theme_minimal() +

p9.theme(

panel_grid_minor=p9.element_blank()

) +

p9.labs(

x="Trading Week",

y="Portfolio Value",

title="Portfolio Value by Investor",

color="Investor"

)

)

Future enhancements include:

- Introducing cash flows (simulating a salary) so agents can distribute new cash

- Introducing more stock tickers

- Introducing qualitative information (headlines, world events)